Febelfin, the Belgian federation of financial institutions, wanted to take on the challenge of digital inclusion. Despite having a strong partner network, they struggled to reach digitally vulnerable communities. We helped them define a concrete strategy during a digital product strategy workshop, using research, stakeholder interviews, and collaborative ideation to identify low-threshold, feasible solutions.

Services

Strategy

Tech

Digital Product Strategy Workshop

Challenge

Febelfin wants to investigate how they can tackle the digital gap between particular communities and digital banking apps. They already have a great network of partners that support digital inclusion and do their part. Next, they want to figure out how they can actually reach communities that are running behind on all things digital.

Our solution

Together with Febelfin, we set up a Digital Product Strategy workshop to figure out what they can do to reach their goal. We started with extensive research to determine the targetted communities' struggles. We gathered this information and used it as inspiration for possible solutions and approaches to this challenge.

Digital inclusion might be a bigger problem than we thought

Febelfin is the Belgian federation of all financial institutions. Recently, they took on the challenge of digital inclusion within the financial sector. The main question to answer is: how do we bridge the gap between particular communities and digital financial banking services?

Did you know that 86% of senior citizens opt out of e-banking because they miss the human touch? We often focus on the elderly, but do you believe us when we say that 39% of our Belgian citizens are estimated to have weak digital skills? Add to this the 7% that isn’t digital at all, and we are at a whopping 46% being exposed to situations of digital vulnerabilities, which is almost one in two people aged between 16 and 74. (King Baudouin Foundation, 2022)

Digitalization is here to stay

The advantages of digital banking are more than clear for all users we encounter daily on our apps. We can barely imagine the situation years ago when we had a cash-only economy or had to do payments from and to accounts at the bank office. The freedom to interact with your bank matters whenever and wherever has become self-evident.

However, even though all transactions are possible nowadays in an entirely contactless manner, this should not come at the cost of completely disconnecting people from their banks. Today the adoption rate of digital banking services is only 81%. (King Baudouin Foundation, 2022)

Febelfin tries to close this gap by helping these people understand and trust the advantages of digitalization and showing them how digital solutions can help them in their daily lives.

Another challenge for digitally vulnerable or excluded communities is online banking fraud. With the increasing ease of use of banking apps comes an increasing responsibility to make our digital solutions safer.

With regular information sessions and courses in local communities, they try to help people with questions and doubts. With this collaboration between Febelfin and icapps, we wanted to find feasible and low-threshold solutions to raise awareness of online fraud for senior users and all digitally excluded or disadvantaged audiences.

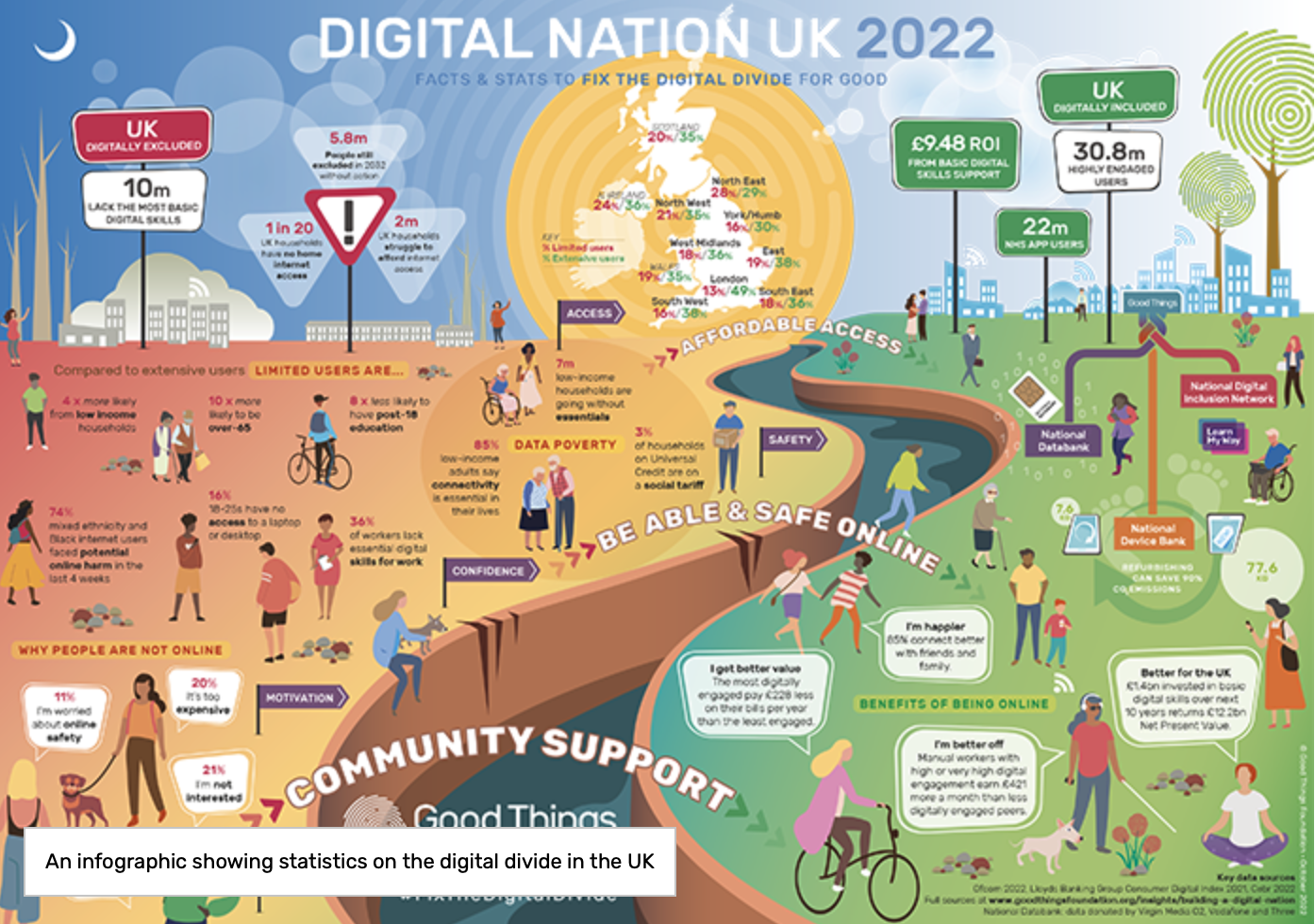

A great example of UK's statistics on the Digital dive

How we managed to guide Febelfin during our Digital product strategy workshop

Since Febelfin wants to take an educational role in digital inclusion, we started by examining its positioning in the market. In other words, how do they reach their target audiences today, what are they trying to achieve, and why. As they often reach their target audiences through third parties, like local initiatives, to teach and advocate the advantages of digital banking, we hit the road and interviewed several of those stakeholders.

We learned what issues are most prominent, what the hardest part of their job is in sending their message to these excluded communities, and how we could help them in their quest for digital inclusion in banking services.

We saw two different paths for Febelfin. Either support third parties in making communication materials on financial fraud and digital banking more easily accessible for caregivers, ‘digihelpers’, and teachers, as too much material is scattered. The second opportunity being ‘how can we help and support individuals directly with accessible-for-anyone and risk-free tools to start daily banking’

With those conclusions, we headed off to our digital strategy workshop to define Febelfin’s long-term goals. Next, we mapped the customer journey of adoption of digital banking solutions, refined with the pain points or challenges these communities experience. And thus pinned down the most difficult moments for them to decide on what opportunity to dive deep.

We thought about how we could turn these challenges into opportunities for improvement by using How Might We’s, a very useful technique to launch brainstorms.

How might we reach the isolated and vulnerable (for digital fraud) people?

How might we remove the barriers to adopting digital banking solutions?

How might we improve digital and financial skills for youngsters in a playful way?

How might we sensitize young people and make them recognize fraud?

We set up several brainstorming exercises after having inspired Febelfin using Lightning Demos with other similar solutions.

The outcome

Febelfin went home with a list of different projects/ideas that can help them execute in the coming months and years to achieve their goals. We also prioritized these items in the list by the value these would create for users and what effort these would require at Febelfin.

This is an example of how our workshops go beyond just coming up with another digital product or tool for your target audience. Our output was tailored to what Febelfin’s target audience needs, and this is not always a digital product. We are happy we could help Febelfin gain more traction, ideas, and enthusiasm to kick-start their project.

Curious what a strategy workshop could do for you?

icapps already has a lot of experience with guiding different customers in the banking industry, which made it possible to speak the same language from the start.